All-in-One

The Employee Lifecycle

All in One Place

From hiring to payroll, connect employee data seamlessly across your organization to maximize efficiency and minimize double entry.

8,134 + reviews

All in One Place

From hiring to payroll, connect employee data seamlessly across your organization to maximize efficiency and minimize double entry.

8,134 + reviews

Trusted by over 10,000 businesses

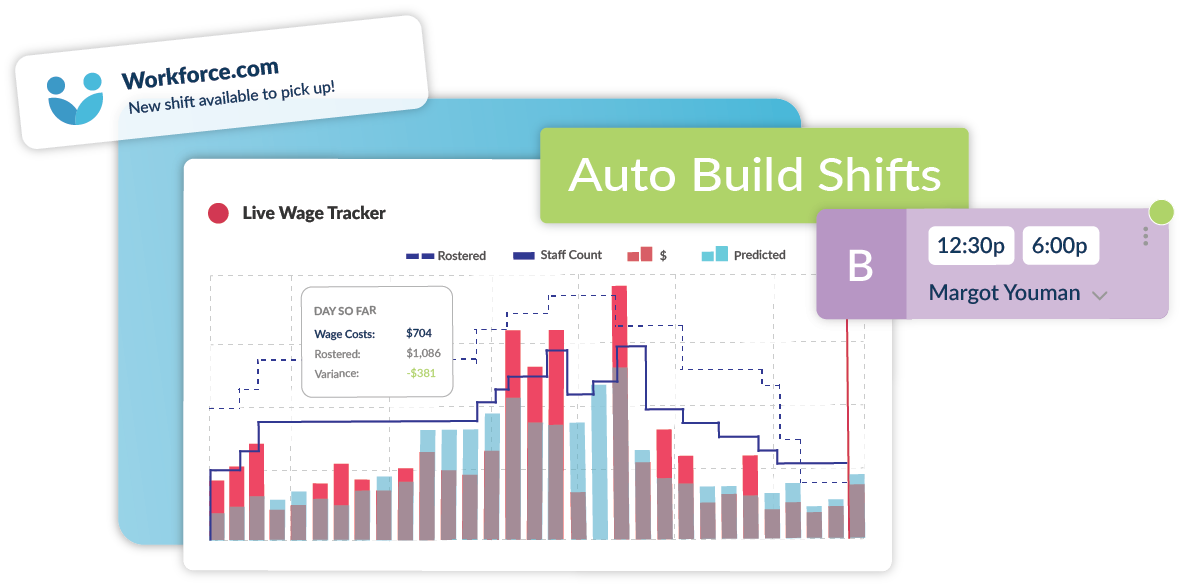

Scheduling

Flexible scheduling driven by AI. Forecast your staffing needs, build schedules efficiently, and react to last-minute changes to cut down on overtime and understaffing.

Click below for a demo

Labor Forecasting

Building Schedules

Shift Swapping

Communications

Human Resources

A single source of truth for employee records. Hire staff and seamlessly onboard them to payroll, eliminating data reentry and freeing up time for performance reviews and engagement initiatives.

Click below for a demo

Hiring

Onboarding

HRIS & Documents

Performance

Management

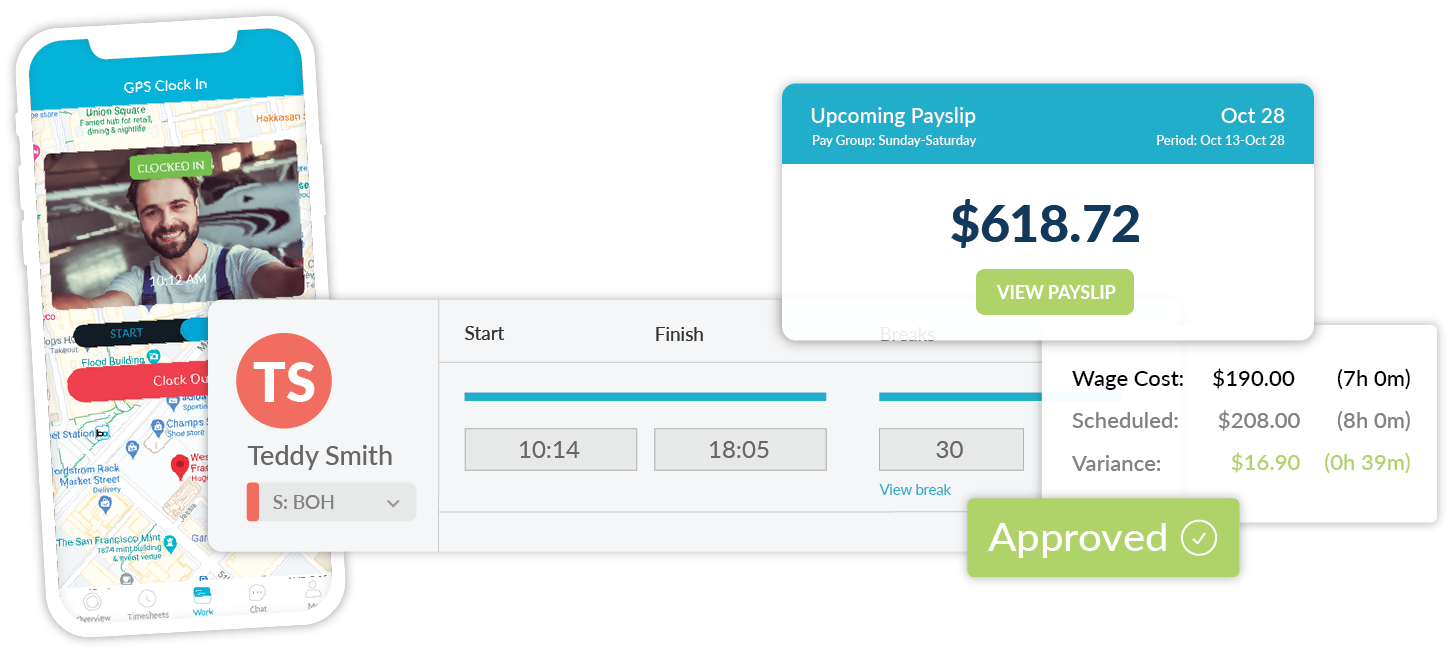

Payroll

Proactive automation for faster pay runs. Daily timesheet approvals, employee portals, and robust wage and tax calculations eliminate common payroll processing bottlenecks.

Click below for a demo

Time & Attendance

Timesheet Approvals

Employee

Self-Service

Payroll Processing